By Marcus Baram, Capital & Main

Property insurance rates have spiked since 2021 due to the increasing frequency of climate-related natural disasters, inflation in the cost of building materials and supply chain issues. The typical homeowner saw an average increase of $648 in their annual premium from 2021 to 2024. And those rates are expected to increase by an average of 8% nationwide this year — with homeowners in some states facing much higher increases, such as a projected 27% hike in Louisiana.

An increasing number of American homeowners are linking those increases to climate change. A majority of them (72%) say that natural disasters such as hurricanes, floods and wildfires exacerbated by climate change are somewhat or very responsible for the rise in homeowner insurance costs, according to a poll by Data For Progress.

There is a bipartisan consensus that prices are rising too fast — nearly 80% of homeowners in Texas, for instance, want to see rates reduced, and one-third of Florida homeowners say that rate increases are the most important issue for them (even ahead of inflation and housing costs) — though Americans are torn on the role of climate change.

Insurance companies are regulated on the state level, and there have been heated debates in states as diverse as Idaho, Minnesota, Louisiana and Colorado about policies and regulations to slow the increase in rates. In Iowa, which was expected to see a 19% increase in home insurance rates this year, nearly 180 researchers and educators signed a statement calling attention to the role of climate change in driving up insurance costs — and calling for better building standards and a faster transition to more renewable energy sources in the state, such as solar and wind.

The federal government plays a role in all this through its funding of programs to share the risk of losses such as the National Flood Insurance Program and disaster relief efforts. It also provides access to climate data used by insurers to foresee potential risks and formulate rates.

The Trump administration’s policies on climate, cutting funding to key programs, reducing access to and limiting the collection of climate data, and slashing the ranks of federal regulators are contributing to an increase in property insurance rates for homeowners, said insurance industry analysts and experts.

“At a time when homeowners are struggling to afford home insurance premiums, the Trump administration has a bunch of policies that are all driving up insurance costs,” said Michael DeLong, the Consumer Federation of America’s research and advocacy associate.

Asked about the Trump administration’s plans to help reduce property insurance rates, a White House spokesperson declined to speak on the record, but provided Capital & Main with a statement from an unnamed official:

“More people are living in Florida than ever before, which naturally causes an increase in rates,” the statement said. “It’s inaccurate and silly to pin this on climate change. The Administration is working to lower costs across all industries for Americans.”

Tariffs

The steep tariffs on materials like lumber, steel and aluminum are raising construction and repair costs, which will likely be passed on to consumers through higher home insurance premiums. First, insurance coverage limits “may no longer provide enough protection as the cost of materials and labor needed to rebuild your home increases,” noted Wawanesa Insurance in a blogpost. “Second, repair costs following claims will be higher, potentially influencing future premium rates.”

The main insurance industry trade group, the American Property Casualty Insurance Association, has been actively lobbying against tariffs because of their impact on home insurance.

Cuts to disaster relief funding and resiliency programs

The administration has cut disaster relief funds at the Department of Housing and Urban Development that are given to local governments and states following natural disasters. The money is used to repair or reconstruct homes and finance housing. Without those resources, communities devastated by such catastrophes won’t be able to rebuild homes and infrastructure in more resilient ways, “and these communities will pay higher insurance premiums as a result,” writes DeLong, the Consumer Federation advocacy associate, and Ethan Weiland, another CFA research associate.

In April the Federal Emergency Management Agency terminated the Building Resilient Infrastructure and Communities Program, which provided grants to states and communities to fund projects that reduce the risk of damage from flooding, tornadoes and other natural disasters. Ending the program “means terminating mitigation projects that would have saved lives, lowered the risk of property loss, and reduced homeowner, farm, and business property insurance premiums,” DeLong and Weiland noted.

Reduced access to critical climate data

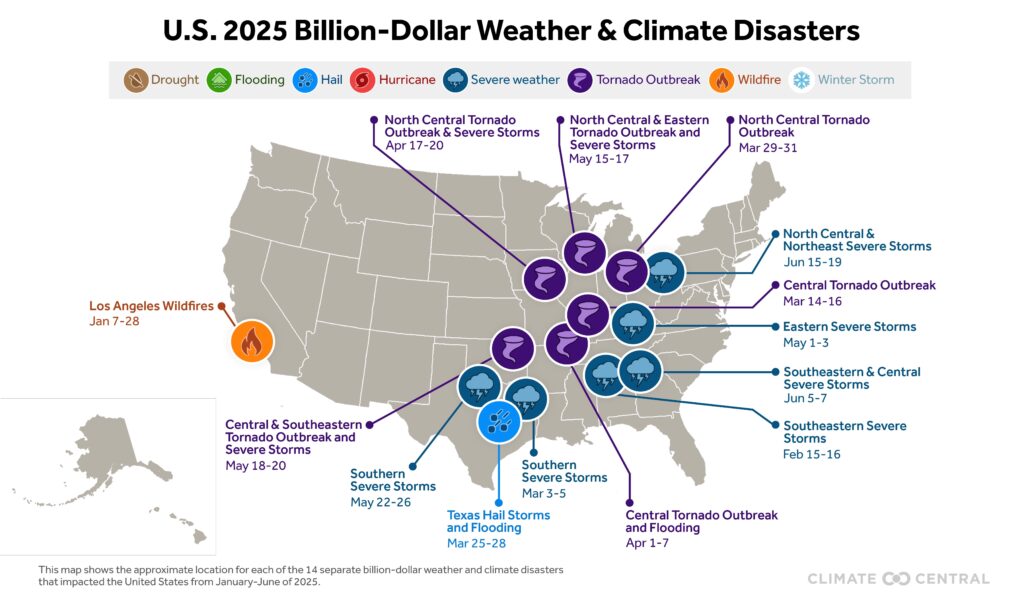

In May, the administration stopped updating the National Oceanic and Atmospheric Administration database for weather and climate disasters that cause more than $1 billion in damage. The database has historically been used by insurance and reinsurance companies to assess risks and project future losses. The loss of that data is likely to lead to less accurate pricing, and cause insurers to hike rates in response to unquantified risk.

In addition, the administration has deleted reports on rising homeowners insurance from the Federal Insurance Office’s website — making it more difficult for insurance regulators, insurers and consumers to get data.

One of the reports, which was uploaded by the Consumer Federation of America, on rising homeowners insurance costs from 2018 to 2022, showed how this increase outpaced the rate of inflation and that policy nonrenewal rates were higher in areas with higher-than-expected losses from climate-related disasters.

“We need reliable, long datasets,” said Kieran Bhatia, head of climate and sustainability for North America at the global reinsurance broker Guy Carpenter. “Without them, you basically are kind of putting your finger up to the wind a little bit about what is a realistic [extreme weather] event.”

Bhatia and other climate risk specialists expressed their concerns during a panel discussion during New York Climate Week in September.

“If you want to promote economic growth, the best way to do that is to have good information,” said Alexandra Thornton, senior director of financial regulation at the Center for American Progress. “Capitalism relies on good information to make an efficient economy and insurers are subject to that rule as well. But now no one has this essential climate information.”

Rollback of renewable energy initiatives

The administration’s rollback of renewable energy initiatives — such as the Environmental Protection Agency’s $7 billion Solar for All initiative — has directly impacted the underwriting market for clean energy projects. That has increased insurance costs as insurers become more cautious about underwriting such projects, citing increased risks.

And President Donald Trump’s executive orders to block state and local climate change measures — such as those that seek to limit carbon emissions or require oil and gas companies to pay for climate damage — could escalate future litigation risk for insurers as climate change worsens.

“We’re going backwards because we’re not doing the things at the federal level to tackle climate change and lower insurance costs for consumers,” Thornton said.

Hindered federal climate risk regulation

Federal financial regulators have withdrawn policies that required climate risk disclosures from financial firms, including insurers, in response to the administration’s anti-environmental, social and governance stance.

By reducing federal oversight, the administration is downplaying climate-related financial risks. This leaves property and financial markets more exposed and increases the instability that can be caused by higher costs and limited insurance availability.

Approval of new fossil fuel projects

The administration’s strong push to increase oil and gas production, such as approving six new liquefied natural gas terminals along the Gulf Coast, will likely accelerate the pace of climate change and lead to higher insurance premiums, said Ethan Nuss, senior campaigner with the Rainforest Action Network.

“The Trump administration’s fast-tracking of dirty energy mega-projects — like the Calcasieu Pass 2 LNG (CP2) methane export terminal — increases the risk exposure of both insurers and neighboring communities that will be stuck paying out larger claims and skyrocketing premiums or be forced out of their ‘uninsurable’ homes.”

This piece was originally published at https://capitalandmain.com/trumps-anti-climate-policies-are-driving-up-insurance-costs-for-homeowners-say-experts. Banner photo: A Florida home destroyed by Hurricane Ian (iStock image).

Sign up for The Invading Sea newsletter by visiting here. To support The Invading Sea, click here to make a donation. If you are interested in submitting an opinion piece to The Invading Sea, email Editor Nathan Crabbe.